Amidst ceaseless mortgage rate hikes and inflationary headlines, the mortgage industry is abuzz with talk of buydowns. Buydowns aren’t a new product, on the contrary, they’ve been around for a long time, but they’re resurfacing now as a mechanism to combat the rising mortgage rates. There are two types of common temporary buydowns, a 2-1 buydown, and a 1-year buydown.

What is a buydown?

A buydown allows a borrower to lower the effective mortgage rate upfront so the monthly mortgage payments are lower during the agreed-upon term. Buydowns work with conventional loans, FHA, and VA loans only, not jumbo loans.

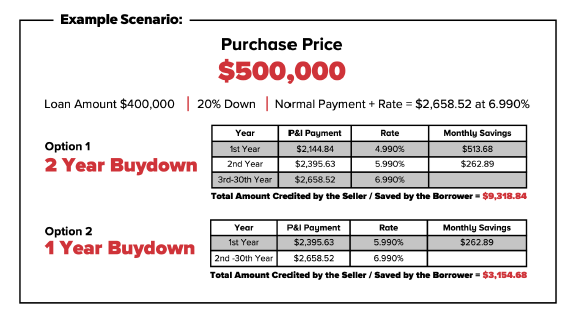

For example, on a $500,000 purchase price with 20% down ($100,000) the borrower must qualify for a 30-year fixed-rate mortgage at the current rate. In this instance, the monthly mortgage payment (principal and interest) would be $2,658.52.

On a 2-1 buydown, in this example $9,318.84 goes into an escrow account at closing. The lender ultimately takes dollars from the escrow account each month during the term of a buydown to cover the difference between the lower payments and what is due. The buyer is then able to pay as if they had a rate that is 2% lower for the first year and 1% lower for the second year, hence the name ‘2-1 buydown.’ The benefit of this escrow account is that the money belongs to the borrower. If rates decrease enough that it makes sense for the borrower to refinance, that money isn’t lost, the money is credited back to the borrower.

Year one, with the 6.99% rate lowered by 2% to 4.99%, the borrower pays $513.68 less every month and year two, they pay $262.89 less than they would with the rate going up 1% to 5.99%. Year three the money in the escrow account has been used towards all eligible payments and the payment goes back up to what it was locked into at closing. The monthly payments rise to what they would have been at the start without a buydown at $2,658.52 and they stay at that level for the remaining life of the mortgage, years 3-30. See example above.

A 1-year buydown is also the same idea only it only lasts 1 year, the payment goes down as if the rate was 1% less and costs less to the seller. See the example above.

What’s in it for the buyer?

The buyer qualifies for the current rate but benefits from a lower monthly payment during the agreed upon term of the buydown. This works for some borrowers who anticipate an income increase during the term of the buydown so that when the buydown ends, they’ll be back up to the full payment with more funds to cover the costs. A borrower may also anticipate mortgage rates to drop within the next couple of years, allowing them the option to refinance to a lower rate before the end of their buydown term. In this case, the buyer would refinance to a lower rate and the remainder of the money from escrow would be applied to the payoff of the original loan.

The caveat is that the buyer and their lender need to have this worked out to the penny before even making the offer as it needs to be included in that as well as the P&S exactly. If these numbers for the seller concession request are off at all in the offer or the P&S, there will be a hold up at closing and put the sale in jeopardy. For a 2-1 buydown the concession is 2.3%, and for a 1 buydown the seller concedes 1.6%.

The buyer may request additional closing costs be credited in addition to the buydown, but can not exceed the allowable maximum seller concession credit for the loan. The closing credit maximums depend on the type of the loan, but they range from 2% to as much as 6%.

- Mass Housing– 3%

- VA– 4% (can cover Funding Fee)

- FHA– 6% (can cover Upfront MIP)

- USDA– 6% (can cover Guarantee Fee)

- Fannie/Freddie: For Primary Residence: o >90% LTV 3%o 75-90% 6% o 75% or less 9% o All investment properties 2%

Why would a seller concede money towards a buyer’s buydown?

Why would a seller give up this money at closing? There are a few potential reasons, the first being that the home just isn’t selling, and they want to attract a buyer without lowering their price. The seller then offers $9,318.84 at closing and sells for $500,000 instead of adjusting the price to $490,000 and they net the full sale price plus that added almost $3,000 they would have lost by dropping to $490,000. Buyers are willing to pay that premium for an easier time making mortgage payments during the buydown and sellers are able to net their desired sale price and get the deal done.

As well, sellers can even use their willingness to work with a buydown in their listing to attract more buyers. Just by putting “Seller would consider a 2-1 buydown concession” in their listing blurb, more agents and buyers could be attracted to make an offer.

This type of buydown is temporary, compared to traditional buydowns where a borrower pays a one-time fee at closing to lower the interest rate for the loan term, which could be 30 years. The traditional rate buydown works differently in this case as that money paid will be lost if the borrower ever refinances during the loan term. The upfront cost is typically much higher as well as it is to apply to the life of the loan instead of the first few years.

As always, mortgage products and programs like these are uniquely beneficial to borrowers depending on many factors. To learn more and determine if this makes sense for you as a buyer or to offer as a seller, contact your expert Realtor today.