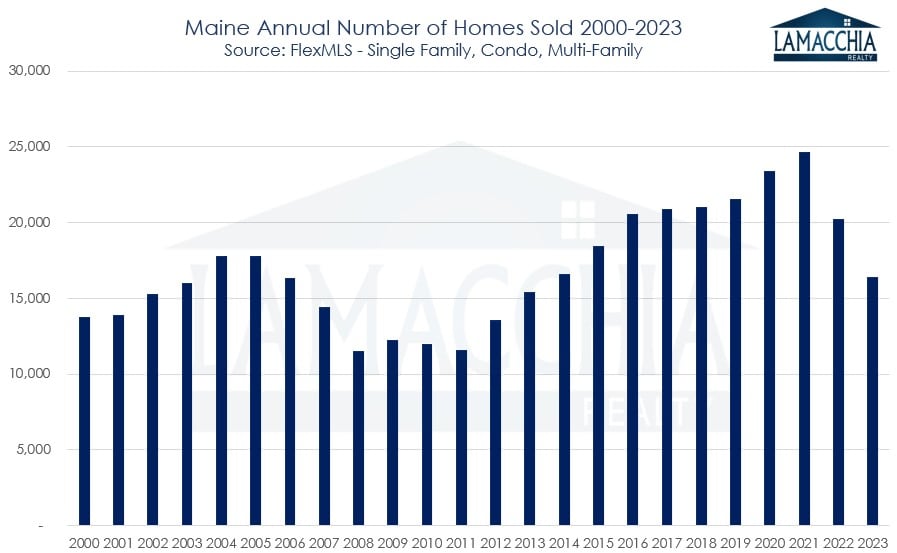

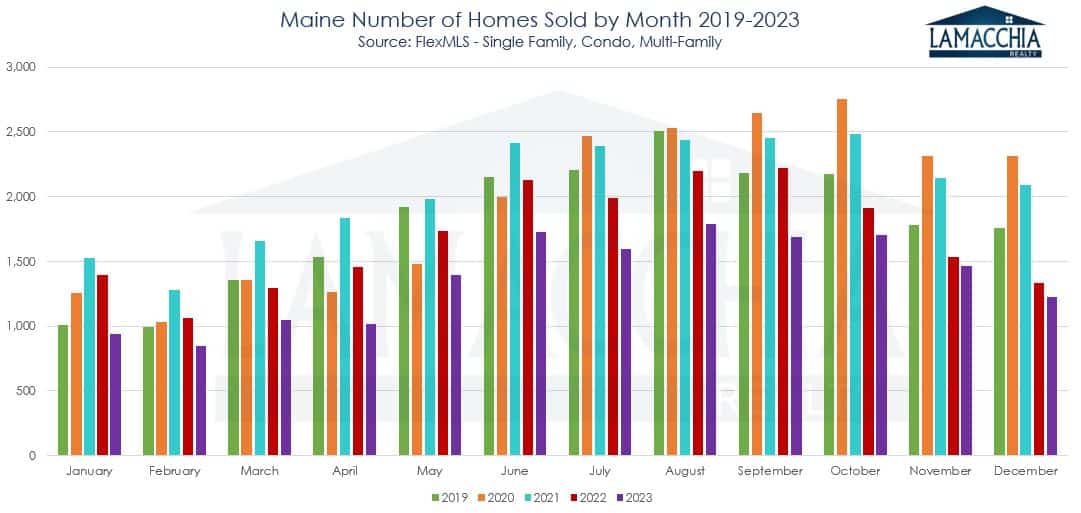

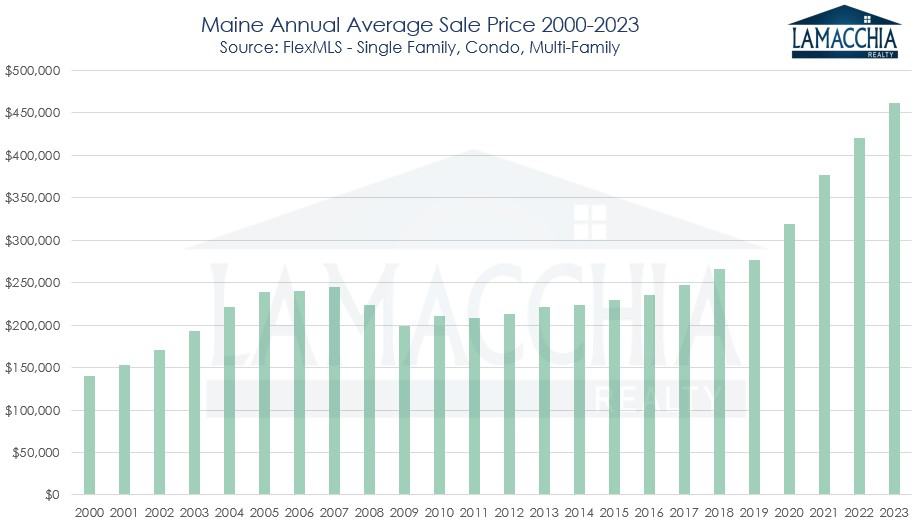

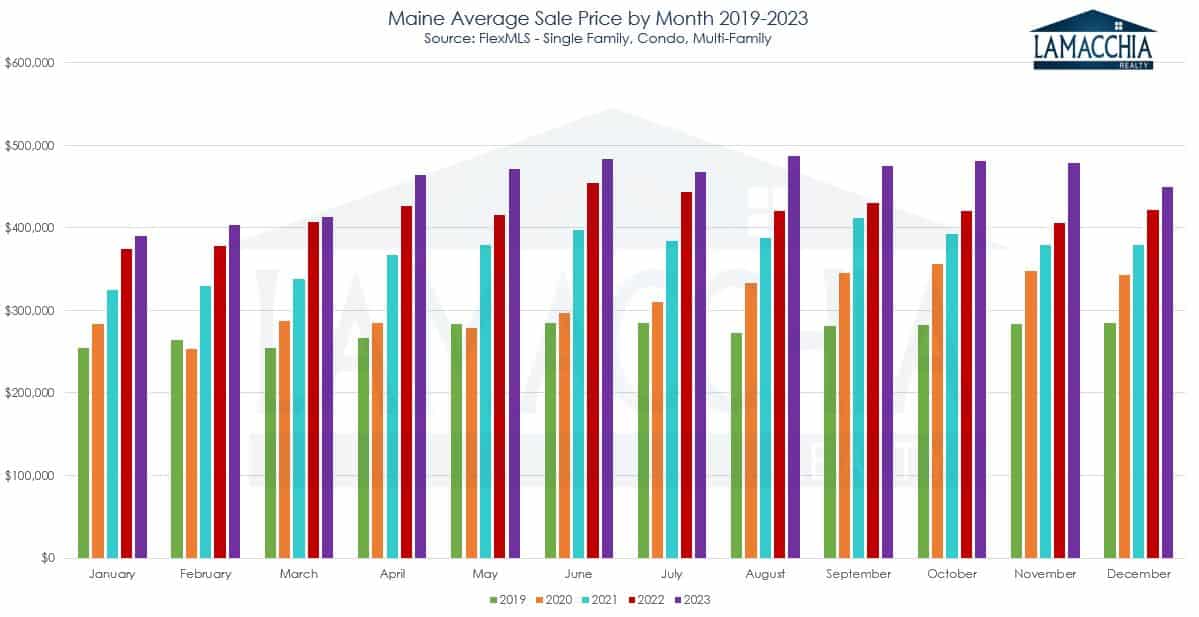

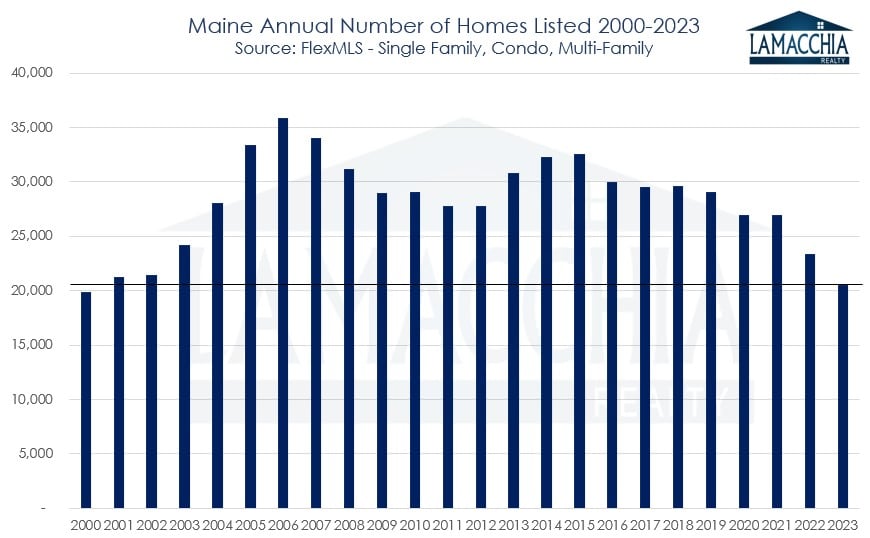

2023 marked a significant chapter in real estate history, on the state level in Maine as well as nationally. If we were to pinpoint the standout factor, it would be the remarkably low number of homes listed, the lowest in over two decades. This scarcity in inventory had the effect of keeping prices high, but there was a substantial decrease in sales, approximately 19%, leaving prospective buyers eager. The attempt to restore equilibrium in interest rates, following their drastic drop in 2020, brought about by pandemic-induced rates, resulted in a sustained presence of higher monthly mortgage payments.

2023 marked a significant chapter in real estate history, on the state level in Maine as well as nationally. If we were to pinpoint the standout factor, it would be the remarkably low number of homes listed, the lowest in over two decades. This scarcity in inventory had the effect of keeping prices high, but there was a substantial decrease in sales, approximately 19%, leaving prospective buyers eager. The attempt to restore equilibrium in interest rates, following their drastic drop in 2020, brought about by pandemic-induced rates, resulted in a sustained presence of higher monthly mortgage payments.

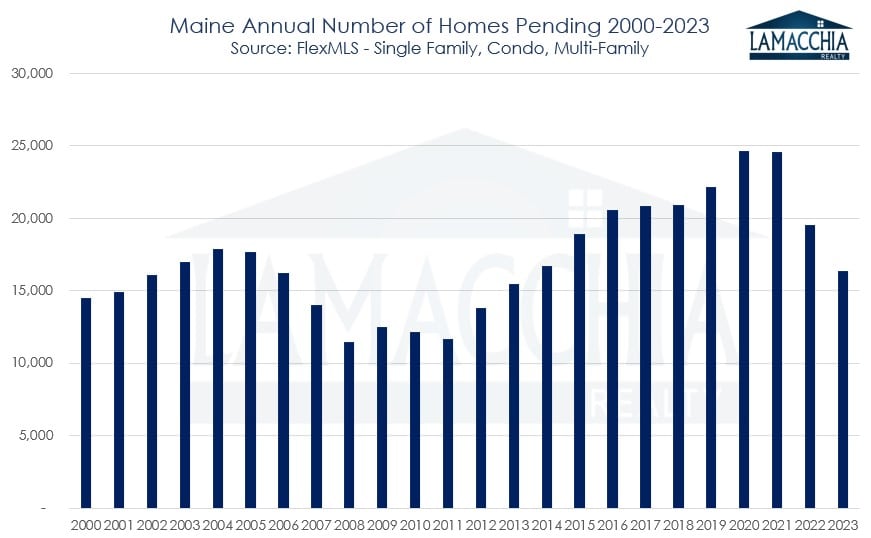

Sales have been adjusting down from the 2021 frenzy for the past few years and when that began, concerns arose that it might be an ominous sign signaling an imminent market crash—a notion Anthony consistently disproved. Fast forward a year, and the anticipated crash hasn’t materialized. This resilience is more attributable to the reduction in inventory rather than a decline in sales. The dip in sales in 2022 wasn’t much of a surprise; rather, it was a welcomed relief. The frenzied market of 2021 was unsustainable, and consumers and REALTORS® alike hoped for a return to normalcy. The slower market activity in the subsequent year reflects the journey back to equilibrium. However, regardless of the necessity of a market adjustment, the process can be painful, and 2023 was certainly uncomfortable.

This report analyzes the sales figures, average prices, the number of active listings, and listings under contract for both 2023 and 2022. Furthermore, it delves into predictions for the real estate landscape in 2024.