First-time homebuyers often debate on whether it’s better to rent or to buy a home. With the current state of the market and the changes to buyer affordability we’ve seen over the last several years, that discussion has only increased. Before the market shift in March 2022, interest rates were lower than ever, but so was the amount of inventory. As a result, any home that came on the market went under agreement faster than ever before, with buyers competing against each other for virtually every home. Now, as interest rates have steadily risen, and overall home prices have increased, we’re seeing less buyers entering the market in the hopes of saving more money if prices cool. Some buyers need to move due to a significant life change such as divorce or relocation, and often consider renting instead of homeownership in those circumstances. What most consumers don’t realize is that rent is increasing as is the cost of living in general due to inflation. Therefore, the ‘more time to save’ idea isn’t really more than just that…an idea.

The Facts

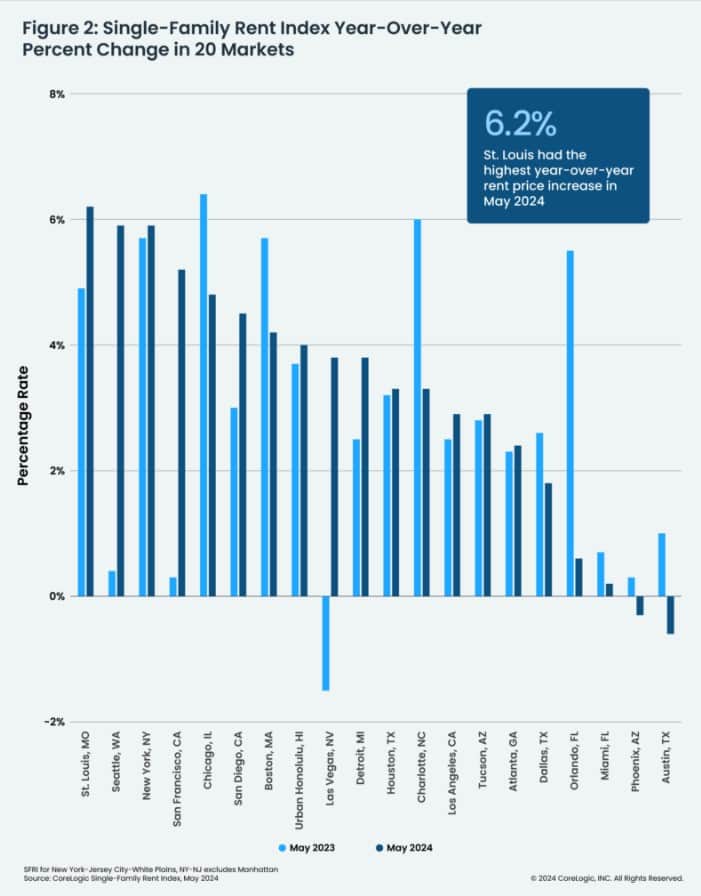

If you’re deciding between buying or renting, let’s take a look at the numbers. There is no doubting that over the past few years, like the cost of all goods, rent prices have risen. According to The Washington Post, national rent prices have climbed nearly 20% since 2019, with the average rent in the United States at $1,712 a month. Additionally, half of all renters in the United States are currently spending more than 30% of their total income on rent and utilities. CoreLogic recently released its Single-Family Rent Index, which looks at single-family rent price changes. For example, the company found that rent for higher-middle priced homes (100% to 125% of the regional median) in the US grew up to 3.3% in May 2024. St. Louis, MI topped the list with the most significant year-over-year rent change of 6.2% compared to 2023.

The Boston area also made the top 20 list of most year-over-year rent change at just under 6% in May 2024. Orlando, FL landed in the #17 spot, and Miami, FL took the 18th spot. The chart below from CoreLogic shows the increase in rent in 20 markets around the country.

Let’s look at the 6 markets Lamacchia Realty focuses on – Massachusetts, New Hampshire, Connecticut, Rhode Island, Maine, and Florida.

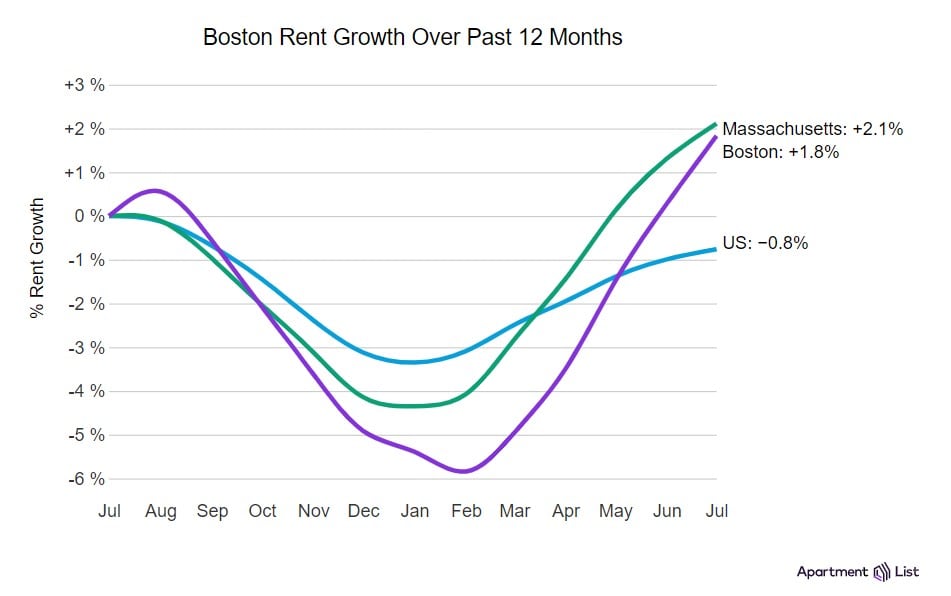

According to apartmentlist.com, rents in Boston alone increased 1.5% compared to last month, with the median rent at $2,366 for a 1-bedroom and $2,491 for a 2-bedroom apartment.

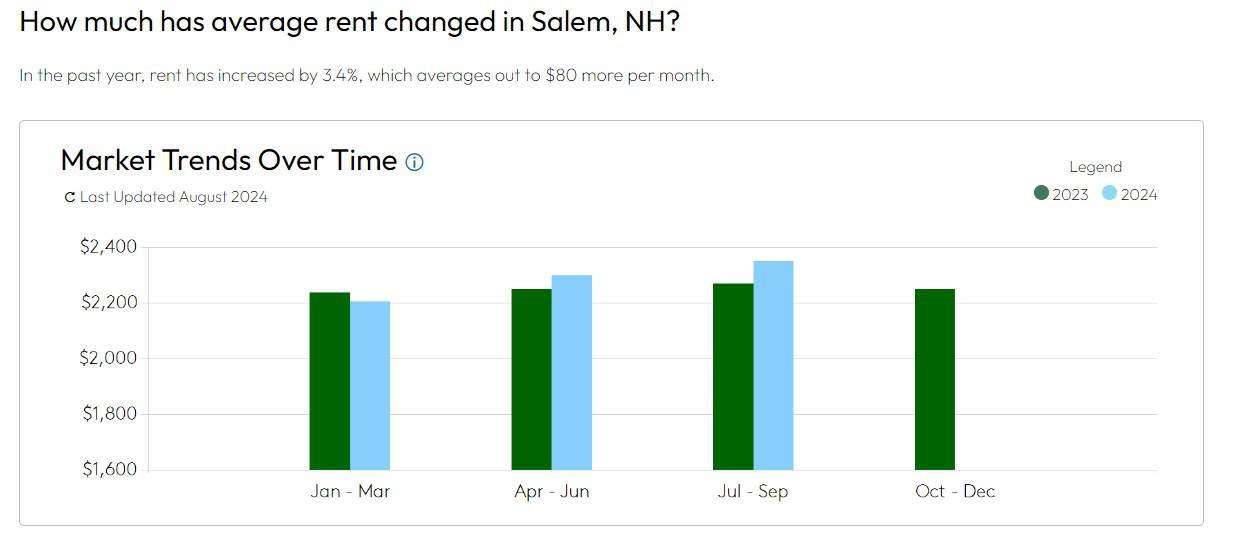

In Salem, New Hampshire, Apartments.com reports that the average monthly rent for a one-bedroom apartment is $2,350, which is a 3.4% increase from last year, making it one of the most expensive cities to rent in nationwide. Studio apartments average at $1,983 a month and two-bedrooms at $2,663 a month.

Those looking to rent in Southington, CT have more affordable options compared to MA and NH. According to Zumper, rent prices have decreased by 7% over the last year. With that being said, the median rent price in Southington still sits at $1,600 a month, with one-bedroom apartments at $1,418 and two-bedroom apartments at $2,257.

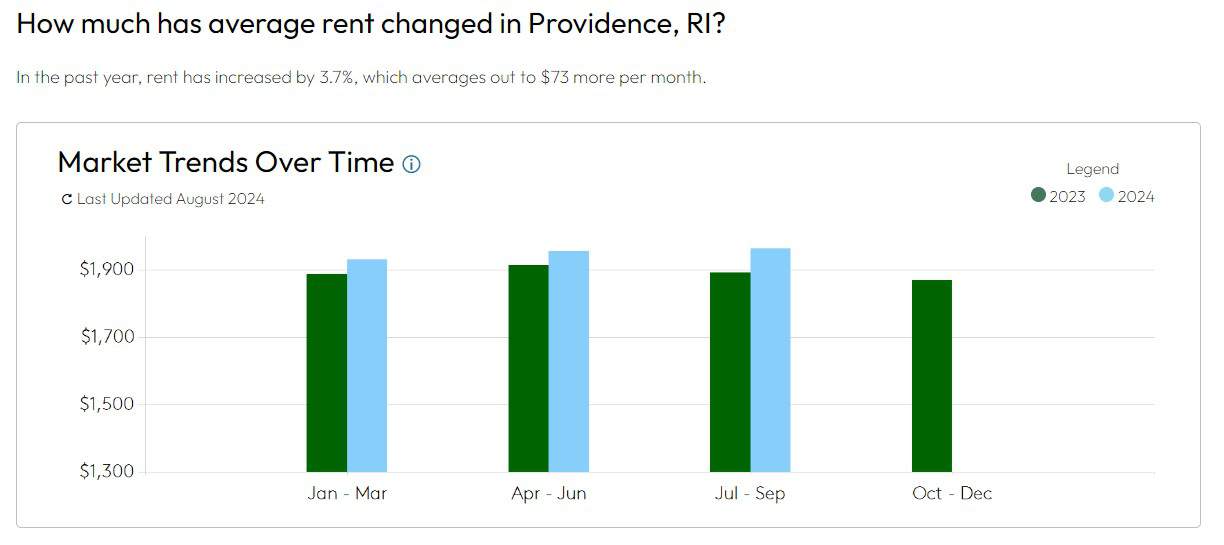

Providence, Rhode Island rentals also saw a rise in price over the last year, according to Apartments.com. The average cost of an apartment increased 3.7% since this time last year, with a one-bedroom apartment averaging at $1,963 a month.

Since Maine has a very small rental market, apartmentlist.com is very limited on how much rental information they can collect for the state. The average starting price for a studio apartment in Maine is $650 a month, and the starting cost for a one-bedroom apartment in Portland sits at about $1,600.

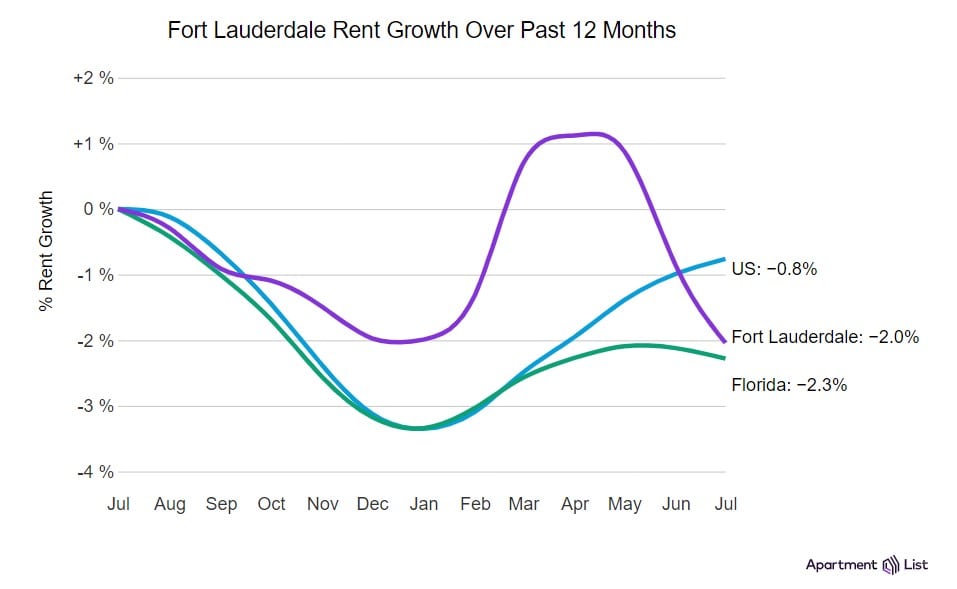

In Fort Lauderdale, according to apartmentlist.com, rent actually decreased in the last month, but only by 1.2%. Rent for a 1 bedroom sits at $1,637 and $2,050 for a two-bedroom.

Why it’s Better to Buy

With all of this being said, most people argue that while rent prices are going up, so are home prices. And while that is true, it’s important to look at where your money truly goes. When you are paying rent, your entire rent goes directly to the landlord’s pocket, but when you own, this goes directly towards paying off the home. In turn, you are building equity, credit, and growing your personal wealth overall.

On top of this, when you buy, you are in complete control of the home. You can make it your own and renovate and design it any way you’d like. When you make renovations, you’re also potentially increasing the overall value of the home. So, if or when you go to sell again, your overall value is potentially more than when you bought it. On top of it all, when you own your own home, you are not tied down to a lease, nor will you have the potential of having a landlord ask you to move out.

Furthermore, when you buy a home, most of the time your rates and payments are fixed – they won’t change unless you refinance depending on the type of mortgage you secure. When you rent, your landlord has the authority to increase rent each year, lessening the amount of money you may be able to save overall. When you buy, you are in control. When you rent, your landlord holds the reigns.

Deciding to Buy a Home? Lamacchia Realty Can Help!

When it comes to renting versus buying, the benefits of homeownership outweigh the latter. From fixed payments to complete control over the home you’re living in, to your payments going directly into the home instead of to a landlord, buying is the right track to take. With the market in a transitional period which will continue for the foreseeable future, it’s important to do your research to truly understand how these changes will impact your home buying decisions.