For this New Hampshire Mid-Year Report, we are focusing on three property types: single-family homes, condominiums, and multi-family homes along with the number of homes listed for sale and placed under contract. This is the first year that we are reporting on the entire state of New Hampshire, as for previous mid-year reports we focused on Belknap, Cheshire, Hillsborough, and Rockingham counties.

The New Hampshire housing market experienced a slightly different outcome than the trends in New England in that sales increased where they decreased in other states, but like New England, prices increased when compared to the mid-year of 2023.

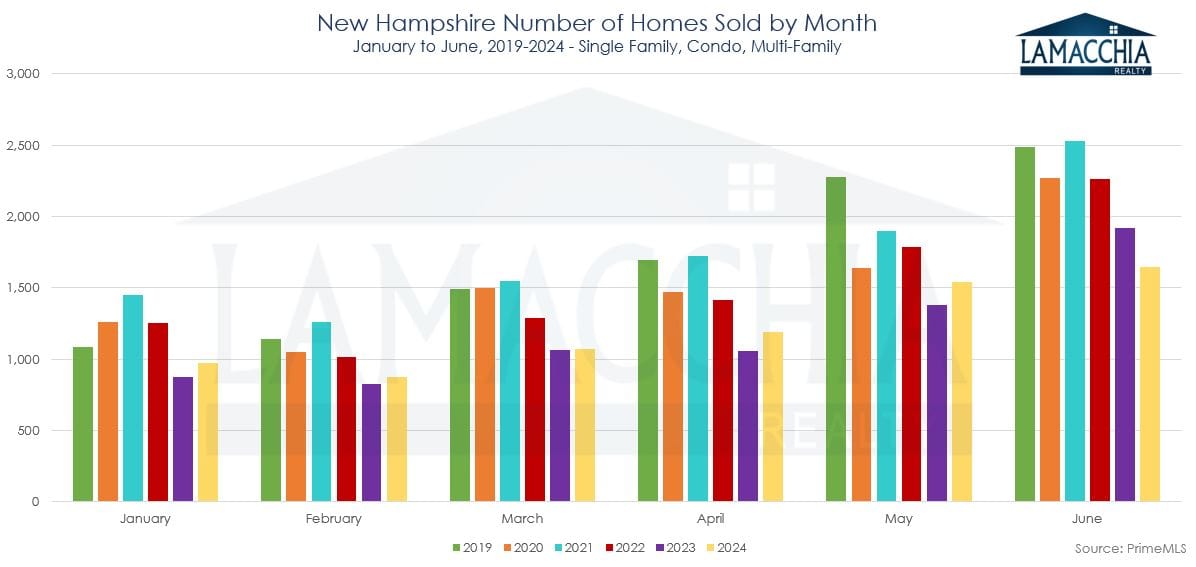

Number of Homes Sold Increased by 2.5%

Home sales increased overall to 7,285 sales compared to 7,110 in the first half of 2023.

- Single family sales increased by 0.6%, condos rose by 9.1% and multi-families decreased by 2.7%.

- With more listings available (see Homes Listed section below), buyers have had a better selection, leading to stronger sales compared to this time last year.

- In the graph below, you can see that monthly sales in 2023 and 2024 were mostly dominated by 2024 resulting in 2024 having an overall 2.5% higher sales. Pre- and post-pandemic sales levels (2019-2022) were significantly higher, and we expect a gradual return to those levels as the market recovers over the next few years.

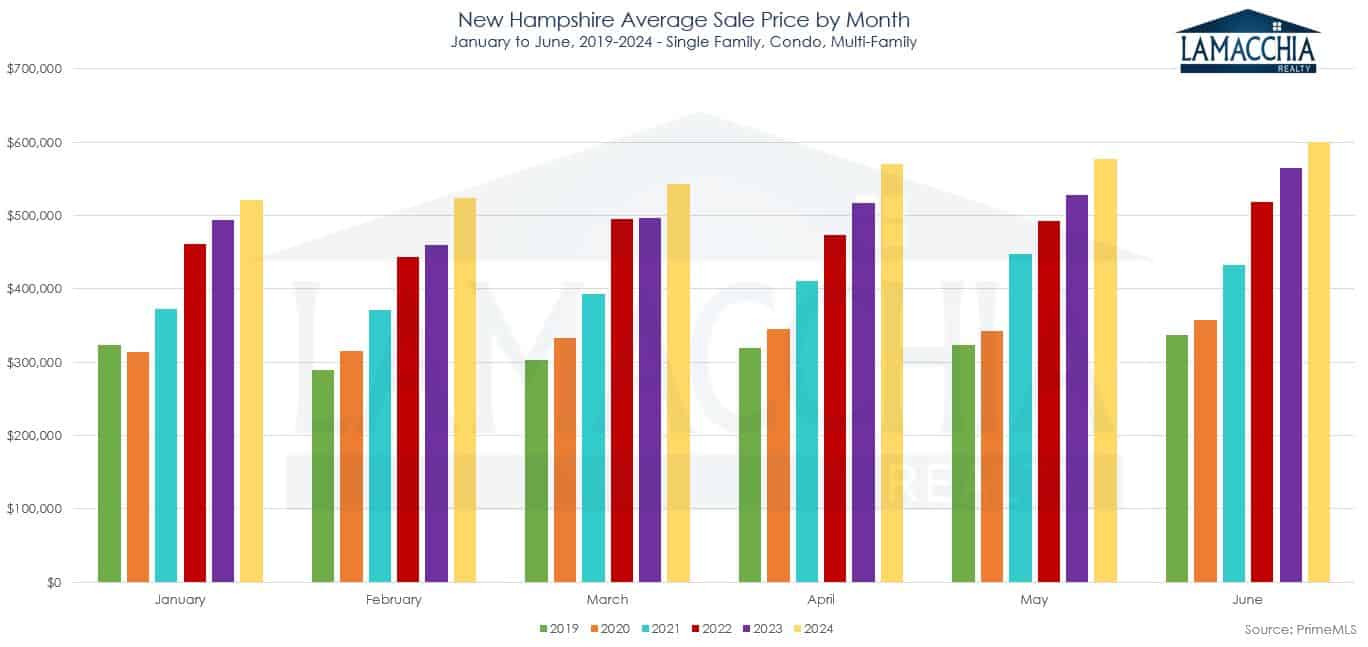

Prices Increase 8.2%

Average prices for homes climbed to $562,344 in the first half of 2024, an 8.2% increase over the same time frame in 2023 at $519,752.

- Prices increased in all three categories: singles up by 8.0%, condos up by 9.6%, and multi-families increased by 12.8%.

- Prices in New Hampshire have been rising for years, with a Covid-era

spike due to high demand. A drop hasn’t occurred due to tight inventory (see the yellow line in the chart to the right) which makes a price drop unlikely.

spike due to high demand. A drop hasn’t occurred due to tight inventory (see the yellow line in the chart to the right) which makes a price drop unlikely. - If high rates are deterring buyers who are seeking more affordable monthly payments, options like mortgage buydowns or mortgage assumptions are worth exploring.

- The chart below shows that monthly prices have steadily increased over the past four years, with 2024 being a record year for New Hampshire.

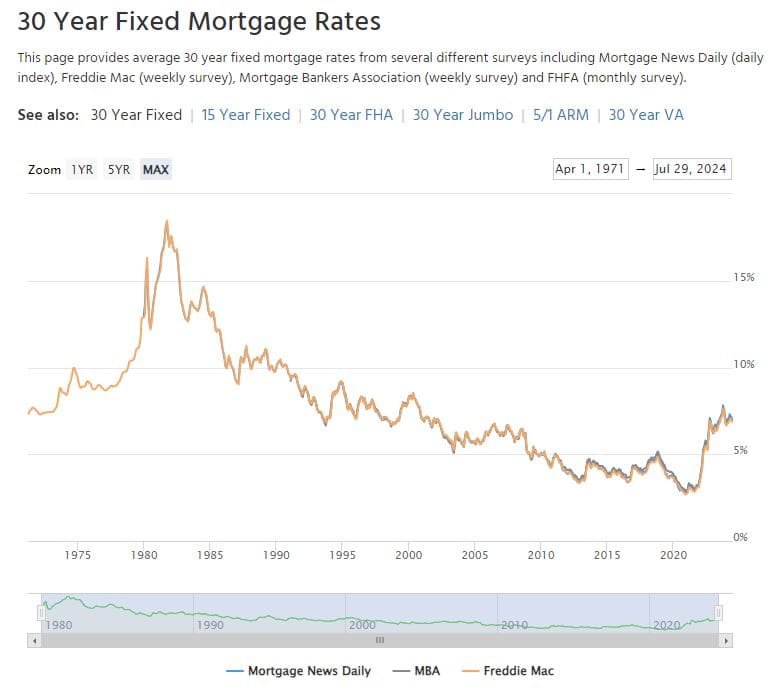

- Recent years of exceptionally low interest rates have distorted our expectations. While today’s rates in the 6%-7% range might seem high, they align more closely with historical norms. As time passes, these rates will likely feel increasingly familiar. Waiting for interest rates to drop before purchasing a home is often counterproductive. Homeownership offers the opportunity to potentially benefit from future rate decreases through refinancing. However, it’s important to remember that rising home prices may outweigh any potential savings from lower interest rates.

Homes Listed for Sale in NH

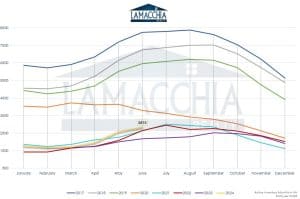

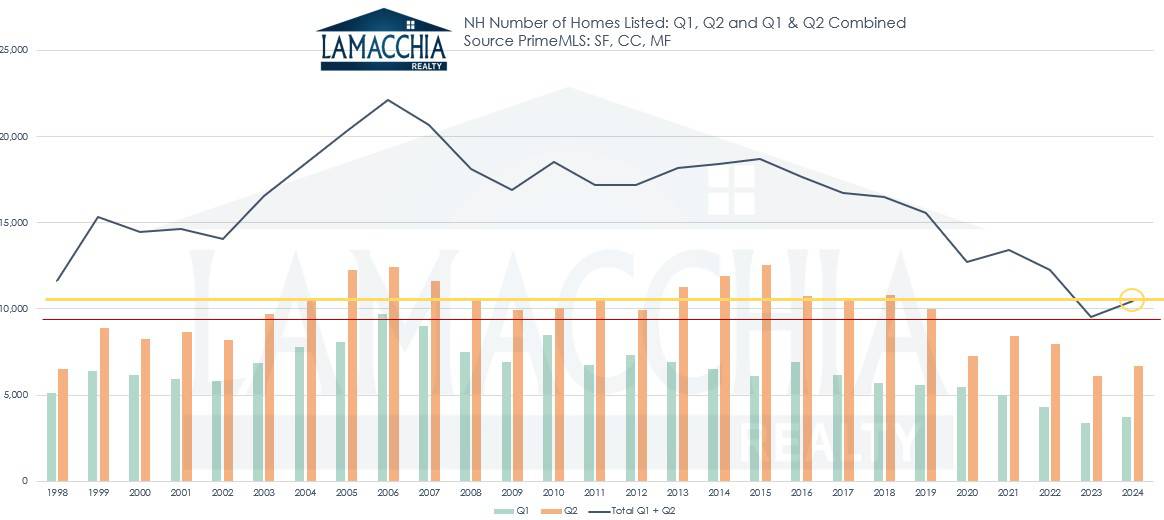

There were 10,462 new listings in the first half of 2024 compared to 9,393 last year, a very welcome 11.4% increase.

- Last year saw the lowest number of homes listed in two decades, indicated by the red line in the graph below. So far this year, listings are higher than last year (yellow line), but still lower than any other year. Overall, this is good news, especially for buyers as this indicates a higher supply.

- Many sellers have been hesitating to list their homes in an attempt to hold onto their pandemic-level rates. However, this rise in listings shows that making moves is not always a choice, especially when faced with certain life changes such as divorce, family growth, empty nesters, relocations, and job/income fluctuations.

- Generally, the number of new listings is an indicator of future pending sales, so with listings number up, we will hopefully see higher pending sales into the fall.

Pending Home Sales (contracts accepted)

The number of homes placed under contract increased by 3% year over year with 9,069 pending sales over 8,808 last year this time.

- More listings and inventory have given buyers more of a chance to buy and therefore, pending sales have risen a bit. However, the increase in pending listings is nominal compared to years past, and the market is still tight.

- Generally, the number of homes pending is an indicator of future closed sales, so we could see a slight rise in sales into the fall.

Predictions for the Rest of the Year

The New Hampshire market outperformed New England in sales and, like New England, exhibited a rise in prices, aligning with earlier predictions.

Many sellers hesitated last year to list their properties due to the low interest rates secured during the Covid era, making it hard to accept current rates of around 7%. These rates are unlikely to change dramatically any time soon and over the past 6 months sellers have begun to move past them and list.

Sellers typically list their homes only when necessary or due to significant life changes. Events such as divorces, expanding families, relocations, and downsizing have driven the market, but these factors haven’t significantly boosted inventory to meet demand. As a result, average housing prices have continued to rise.

Buyers are determined to find homes within their budgets, now lower due to rising rates and prices. Monitoring rates and keeping pre-approvals up-to-date is crucial to be ready to strike if rates drop.

Homeownership offers advantages over renting, including full control over your living space, fixed monthly payments, and asset growth through equity. Mortgage interest is often tax-deductible, especially in the early loan stages.

At mid-year, sellers face varied market conditions. The first half of the year tends to favor sellers, while the second half leans towards buyers. Listing your property now can still be beneficial. Setting a competitive price can attract more buyers and give you greater control over negotiations. Sellers should not wait, as hoping for lower rates might mean missing out on the perfect home. If rates drop and prices remain steady, refinancing can help secure a lower interest rate.

National factors affecting the market include commission changes and the election. The commission class action settlement will alter how real estate commissions are handled, causing some confusion. Starting in August, sellers may only need to pay their agent’s commission, while buyers will cover their agent’s fees out of pocket. This change would have impacted VA buyers, but a temporary amendment allows their benefits to continue. Buyer affordability might be affected since this fee can’t be included in the mortgage. The election year may slow down the real estate market this winter, but a faster-paced market is expected in 2025 once the changes settle.

Data provided by PrimeMLS then compared to the prior year.