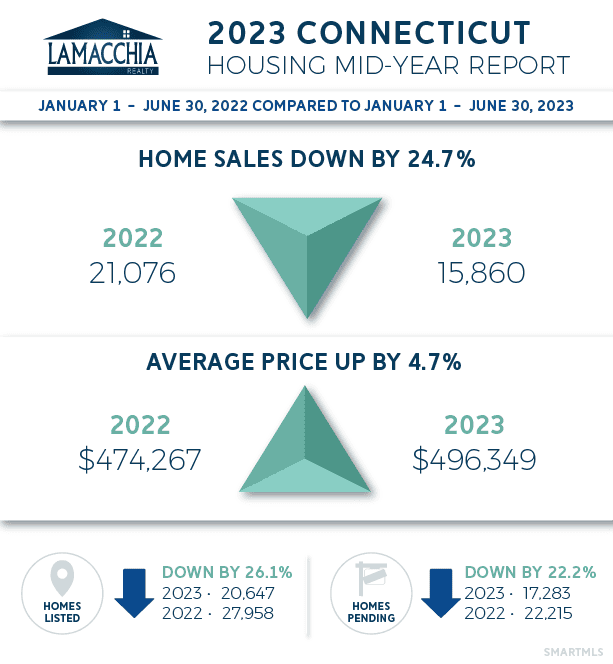

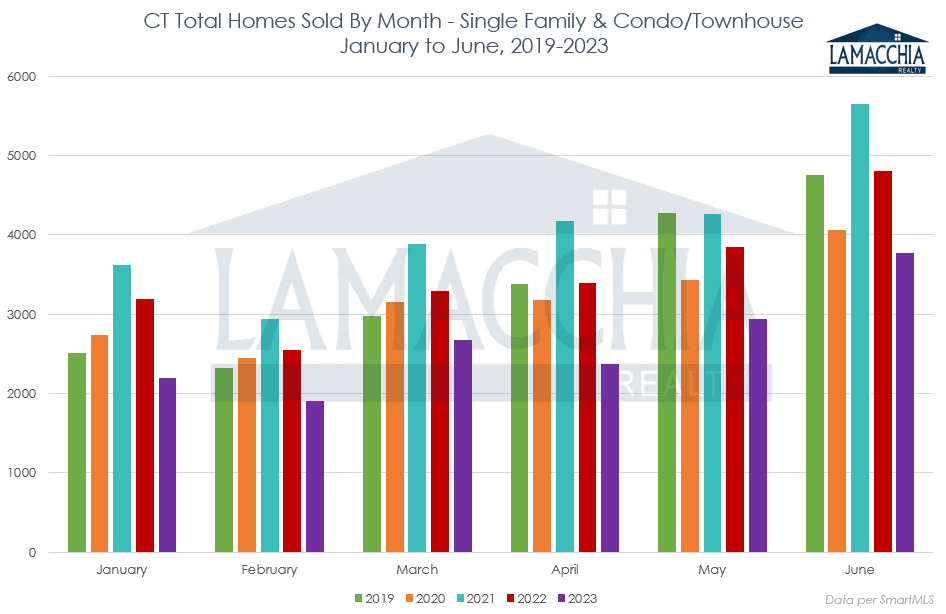

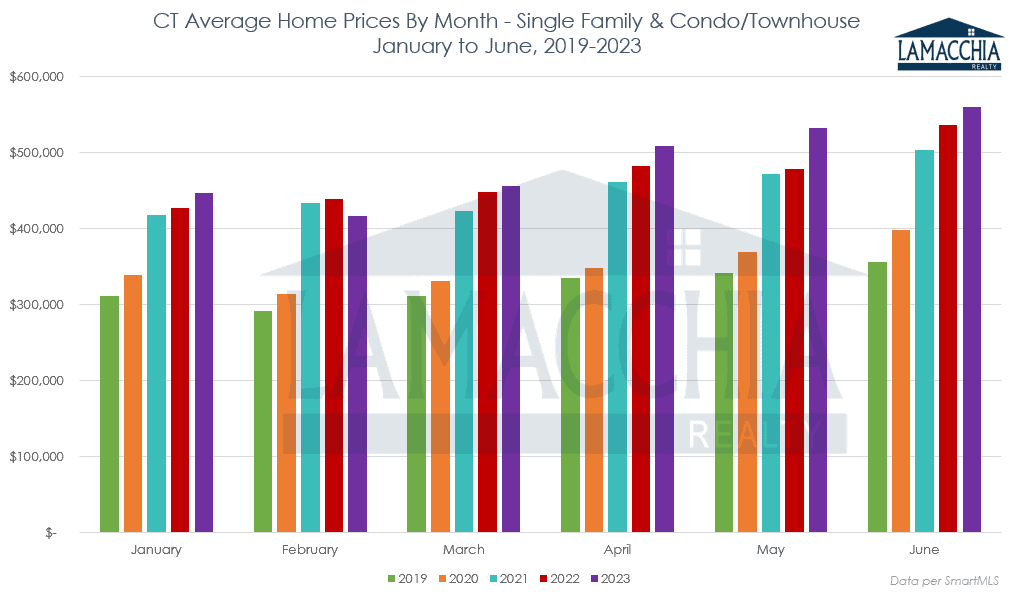

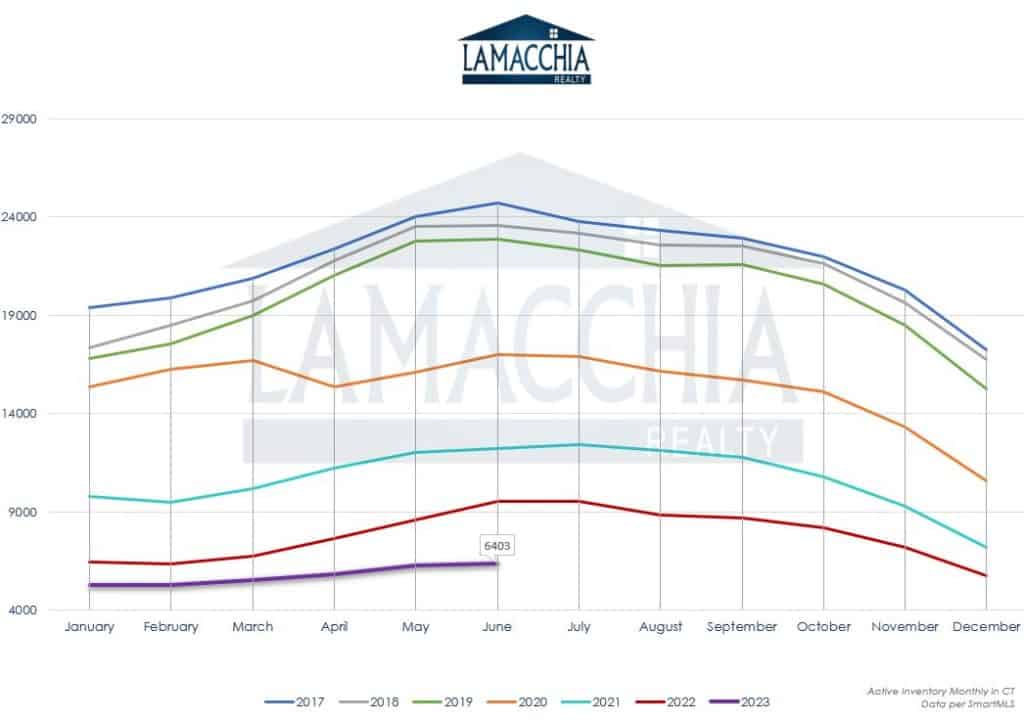

Like other New England states, and pretty much nationally, the Connecticut market has seen a decline in sales coupled with a rise in prices, which aligns with our earlier predictions but in this state is experiencing extra pressure on available inventory.

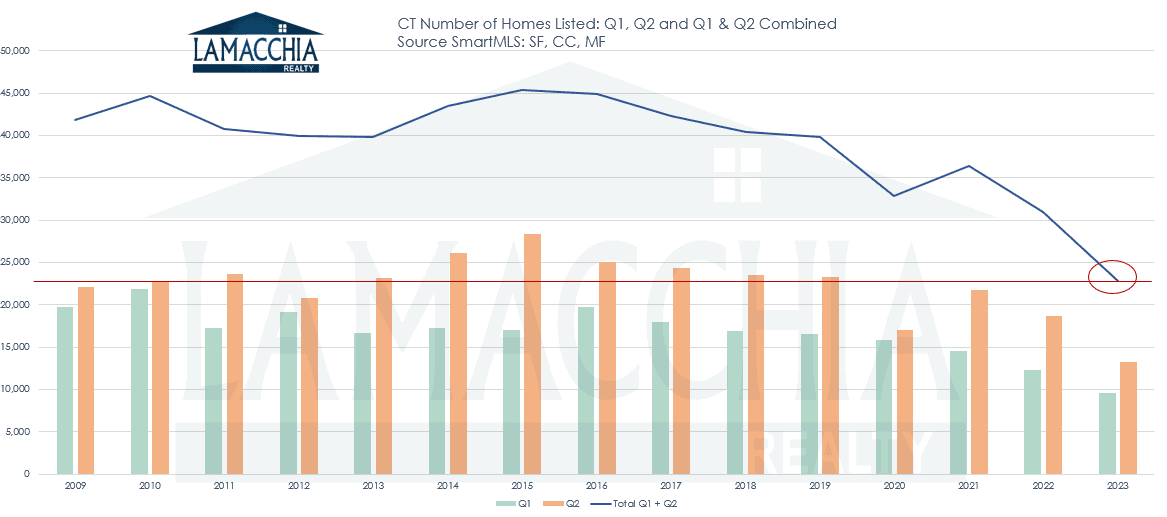

Many sellers are reluctant to list their properties due to the low-interest rates they secured during the Covid era, making it difficult to accept the current rates of around 7%. It is likely rates will stay at this level for at least the next few months and therefore, we also expect that we are going to finish the year with the least amount of homes listed in recorded history.

Only when faced with necessity or significant life changes are sellers compelled to put their homes on the market. Events such as divorces, expanding families, relocations, and downsizing have driven the market, but even these factors have not been enough to boost inventory with an adequate number of homes to meet demand. As a result, housing prices on average have remained on the rise.

Buyers actively searching for homes are determined to find the perfect match that fits their requirements and budget, which is now lower than last year due to increasing rates and prices. This reduced affordability underscores the importance of monitoring rates and maintaining up-to-date pre-approvals. If a drop occurs, buyers are urged to promptly update their pre-approvals, so they can be ready to strike if the opportunity arises.

As we reach the mid-point of the year, sellers encounter favorable and unfavorable market conditions. Traditionally, the first half of the year favors sellers in what is known as a seller’s market. However, for those simultaneously selling and buying, the latter half of the year typically shifts towards a buyer’s market, making it still advantageous to list your property now. To succeed in this market, setting a competitive price for your home is essential. Attracting a larger pool of potential buyers provides you with increased leverage, affording greater control over negotiation terms such as timing, contingencies, and price.

Given the current low inventory and stable prices, a housing price crash is not anticipated anytime soon if at all. Anthony has described this market as similar to the 1980’s with low inventory and consistent prices. While interest rates have increased compared to the pandemic period, historically, their level is relatively moderate. Many believe that in the long run, rates around 5-6% will be the norm. Considering this perspective, sellers should not delay selling and moving into a new home, as waiting for the time for significantly lower rates might keep you waiting and missing out on the perfect home. Alternatively, if rates do decrease and prices continue to remain steady, refinancing could be an excellent opportunity for sellers to secure a lower interest rate if a drop occurs.